Home Renovation Loan - Questions

Home Renovation Loan - Questions

Blog Article

Some Ideas on Home Renovation Loan You Should Know

Table of ContentsThe Of Home Renovation Loan3 Simple Techniques For Home Renovation LoanGetting The Home Renovation Loan To Work9 Easy Facts About Home Renovation Loan ExplainedWhat Does Home Renovation Loan Mean?

Assume you additionally take right into account the decreased rate of interest on this lending. Consider a house remodelling car loan if you want to restore your home and give it a fresh look. Banks give loans for home owners who wish to restore or improve their homes yet need the cash. With the help of these lendings, you might make your home more cosmetically pleasing and comfortable to reside in.There are plenty of funding options offered to aid with your home renovation. The best one for you will rely on just how much you require to borrow and just how quickly you want to pay it off. Brent Differ, Branch Supervisor at Assiniboine Cooperative credit union, supplies some useful recommendations. "The initial point you should do is get quotes from several contractors, so you know the fair market value of the work you're getting done.

The major benefits of utilizing a HELOC for a home remodelling is the versatility and low rates (typically 1% over the prime price). In addition, you will only pay interest on the amount you take out, making this an excellent choice if you need to spend for your home improvements in phases.

The primary drawback of a HELOC is that there is no set payment schedule. You need to pay a minimum of the rate of interest monthly and this will raise if prime prices go up." This is an excellent financing option for home improvements if you wish to make smaller sized regular monthly repayments.

The Of Home Renovation Loan

Given the possibly lengthy amortization period, you might wind up paying significantly more rate of interest with a home mortgage refinance contrasted with various other funding alternatives, and the prices related to a HELOC will certainly additionally use. home renovation loan. A home loan re-finance is successfully a brand-new mortgage, and the rates of interest could be more than your existing one

Prices and set-up costs are commonly the like would spend for a HELOC and you can repay the funding early without penalty. Some of our customers will begin their renovations with a HELOC and after that change to a home equity financing as soon as all the costs are confirmed." This can be a good home remodelling financing choice for medium-sized jobs.

Personal loan rates are typically greater than with HELOCs typically, prime plus 3%., the major disadvantage is the rate of interest price can commonly vary in between 12% to 20%, so you'll want to pay the equilibrium off quickly.

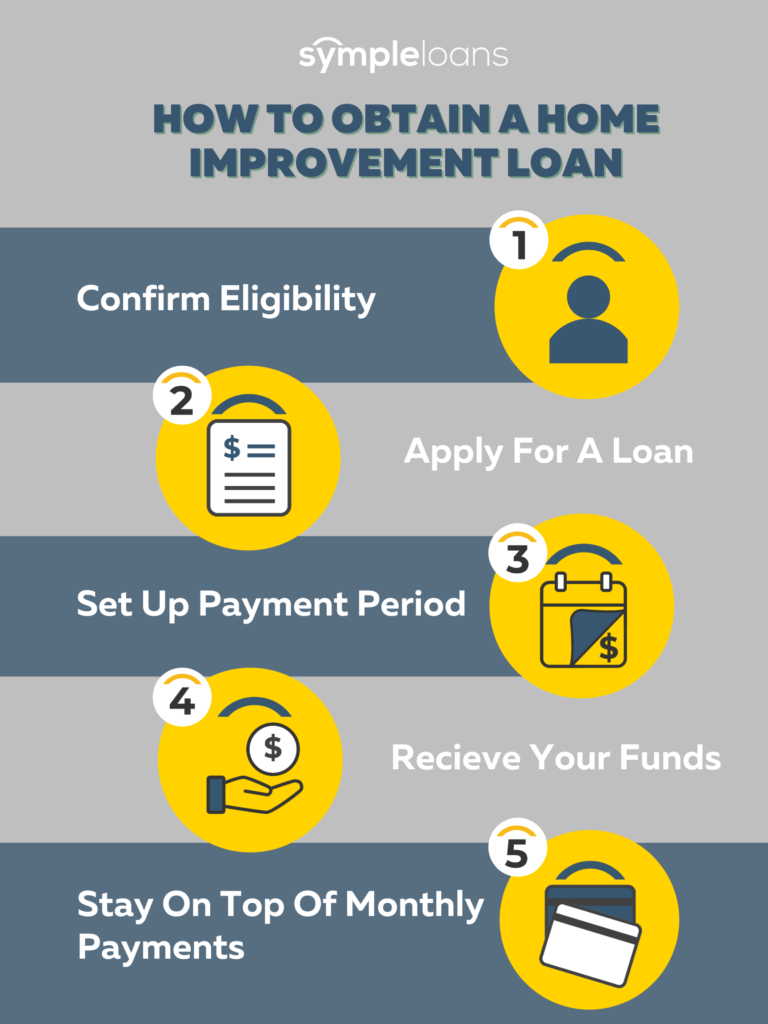

Home restoration car loans are the funding choice that permits home owners to refurbish their homes without having to dip into their financial savings or splurge on high-interest credit cards. There site here are a range of home renovation lending resources offered to pick from: Home Equity Line of Credit Scores (HELOC) Home Equity Lending Home Mortgage Refinance Personal Loan Charge Card Each of these funding choices features unique needs, like debt rating, proprietor's income, credit line, and interest prices.

Excitement About Home Renovation Loan

Before you start of creating your dream home, you most likely want to understand the a number of kinds of home remodelling loans readily available in copyright. Below are some of the most typical types of home restoration loans each with its own set web of attributes and advantages. It is a kind of home renovation car loan that enables house owners to obtain a bountiful amount of cash at a low-interest price.

These are beneficial for large-scale renovation projects and have lower interest rates than various other types of personal finances. A HELOC Home Equity Line of Credit report is similar to a home equity financing that utilizes the value of your home as safety. It operates as a charge card, where you can obtain as per your needs to fund your home renovation tasks.

To be eligible, you must possess either a minimum of a minimum of 20% home equity or if you have a home mortgage these details of 35% home equity for a standalone HELOC. Re-financing your home loan process entails changing your current home loan with a brand-new one at a lower rate. It minimizes your monthly repayments and lowers the amount of rate of interest you pay over your lifetime.

The Ultimate Guide To Home Renovation Loan

For this, you might require to give a clear building plan and allocate the remodelling, consisting of determining the cost for all the products required. Additionally, individual financings can be secured or unsafe with shorter payback durations (under 60 months) and included a greater interest price, depending upon your credit history and earnings.

Indicators on Home Renovation Loan You Need To Know

Store funding programs, i.e. Installment plan cards are provided by several home renovation shops in copyright, such as Home Depot or Lowe's. If you're preparing for small home improvement or do it yourself projects, such as setting up new home windows or washroom remodelling, obtaining a shop card via the store can be an easy and quick process.

Report this page